α🥬#38 - Bitcoin Hits 40k, Looks Toppy.

α🥬#38 - Bitcoin Hits 40k, Looks Toppy.

Weekly Crypto Market Insights

Hi and welcome to α🥬 a (mostly) crypto-focused weekly newsletter.

Today on the menu:

Bitcoin hits $40k!

Crypto Assets & Rehypothecation

…and some fun bits and bytes!

DISCLAIMER: This content is not financial advice and only represents my personal opinions.

Always do your own research.

Bitcoin.

So this happened yesterday:

Bitcoin broke above $40k for the first time in its history.

It’s been the wildest of year in the market and bullish news about institutional/corporate involvement have accumulated. At the same time, the US regulator cleared the way for banks to custody crypto assets and to process payments on public blockchains.

While the narrative for most of 2020 was that of institutional involvement, it now looks like retail is rushing back into the market.

As a consequence, the market is experiencing very rapid parabolic price action which screams correction to me.

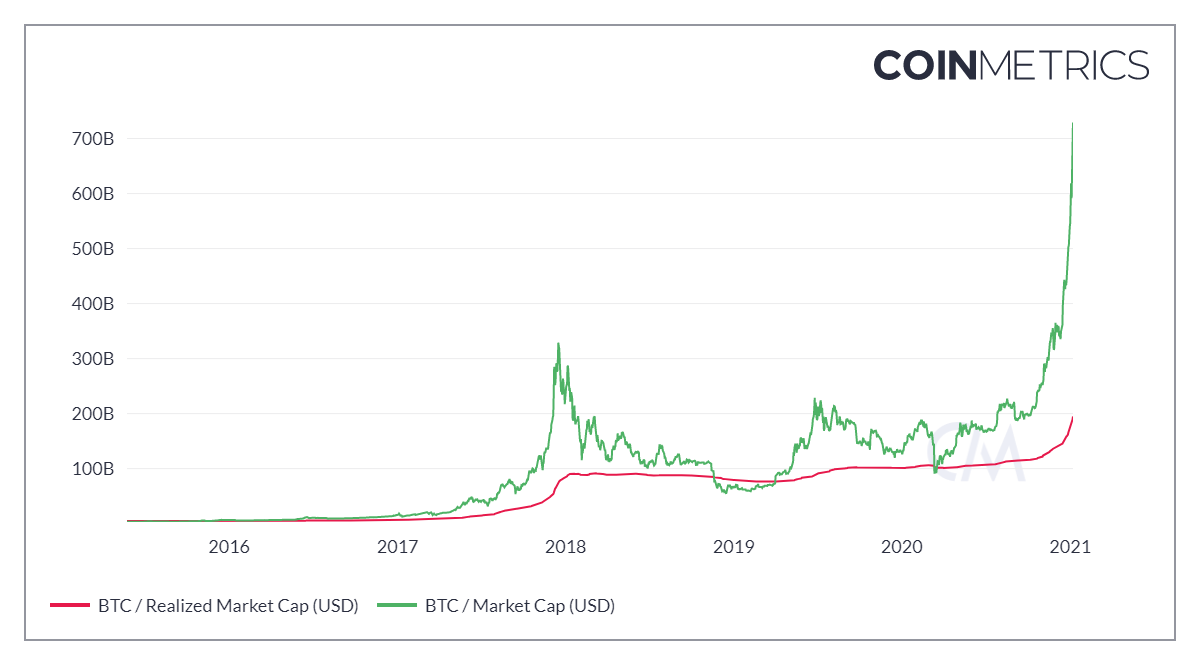

I mean, look at this chart:

The ratio Market Cap to Realized Market Cap (aggregate cost basis of bitcoin holders) is around x3.75 which means that your average smart money BTC hodler is about +375% in profit in the current cycle.

At some point (which I believe will be soon), the market is going to run out of new money and the profit taking will start. You can then expect equally big candles on the downside.

So, my advice if you can’t wait to get into bitcoin is:

Patience.

Let the market cool down and correct before you get in, chasing the momentum will put you at risk of being the biggest fool.

Here’s a proven strategy and how you should think about investing into Bitcoin.

Think about Bitcoin as a very volatile saving account in cyberspace. You want to allocate to it consistently (like, say, every month) but in reasonable increments (only a fraction of your monthly earning at the time). This strategy is called dollar-cost-averaging and it’s proven to be extremely profitable in the long run because, well, numbers go up! just in a very volatile fashion.

So again, this is no time to mortgage the house to get into Bitcoin. Be disciplined, have an investment plan and stay away from day-trading!

Bitcoin and Assets Rehypothecation.

I recently got into the rehypothecation rabbit-hole to try to understand how it would work for crypto assets.

Rehypothecation is defined in this IMF research paper as:

“[A]ny use of client assets by a financial intermediary”.

In a typical re-hypothecation transaction, securities that serve as collateral for a secured borrowing (e.g. a margin loan extended to a hedge fund) are further used by the dealer or bank making the loan.

Frequently, the collateral taker in the first transaction pledges the securities to one or more third parties to obtain financing to fund the margin loan or uses them to facilitate other transactions for clients (e.g. short sales).

In some instances, where permitted by the relevant regulatory regime, financial intermediaries may use client securities to finance other activities not directly related to clients, including inventory or proprietary trading positions.

In traditional finance, rephypotheciation is useful because:

[It] supports the flow of collateral as well as funding liquidity, and therefore helps to bring liquidity to where it is most needed. [Rehypothecation] allows firms to raise more financing than would otherwise be possible and can contribute to the liquidity of securities’ markets.

In crypto, rehypothecation is, well…. problematic.

Typically it can be done by lending desks like BlockFi. You give them your bitcoin, they lend it to third-party firms and you get some interest in return. The interest rate represents the risk you’re taking for allowing BlockFi to rehypothecate your coins.

Now, what happens if that third party also decides to re-use the Bitcoin (lent to them by BlockFi) and lend it to another third party.

In this case you end up with a chain of rehypothecation.

In traditional finance, such chains are extremely common. A treasury bill might end up being rehypothecated multiple times. And each time the borrower will write the bill as an asset on their balance sheet. This creates situations where the same asset might be “owned“ by 4 or 5 entities and being collateral to multiple loans.

At scale, this system can cause enormous risk because if a big enough number of lenders call back their collateral at the same time (say, to liquidate them to get cash), it can lead to cascading defaults on loans and liquidity crunches.

According to Jeff Snider, this is exactly what caused the fall of Lehman back in 2008.

Fortunately, such events can be backstopped by central banks. Since central banks can “print” money indiscriminately, they can always act as a lender of last resort, inject liquidity to chocking markets an save the day.

As you might imagine, this doesn’t work for Bitcoin.

The reason is that there is no lender of last resort in Bitcoin. Bitcoin’s supply is completely inelastic, i.e. it doesn’t go up when demand goes up and central banks cannot just print a bunch of coins to relieve markets.

If something goes wrong and prompt creditors to call their Bitcoin back, you better have the BTC or you’ll go down.

This is what happened to crypto lending platform CRED a few months back. Turns out they used their depositors’ bitcoin to extend outrageous 40% interest micro-loans to Chinese retailers (wtf!). When those loans defaulted, they weren’t able to make good on the Bitcoin and ended up with a giant whole in their balance sheet. Bankruptcy ensued.

Solutions exist though.

Long would go on to found Wyoming Crypto Bank Avanti which is legally prohibited from creating leverage on crypto deposits.

This of course brings us to philosophical questions about what the world would look like if all we had were crypto banks that were prohibited to leverage their deposits.

In my humble opinion, the economy needs a certain amount of waste to function well. This is why I don’t see traditional banks an assets disappearing anytime soon.

If you’d like to go deeper on the issue of rehypothecation in crypto, I suggest you take a look at this discussion between Caitlin Long and Dr. Manmohan Singh, the IMF’s leading expert on rehypothecation and shadow banking.

Bits and Bytes.

What if Bitcoin actually were a “fictional substance in an ongoing and massively coauthored book“. Uh! I mean, why not?! Well, this nutty but fascinating idea is explored in this paper by Northern Illinois University philosopher Craig Warmke 🤔

Hasu, Su Zhu and Arthur_0x discuss the 20 most prominent projects in DeFi in this two-part conversation (1 - 2), these guys have been on top of the DeFi space for a couple years so you can definitely get some good alpha there.

Jack Ma has been missing since calling China top bankers a “club of old people“.

Lyn Alden has produced yet another monster article titled The Fraying of the US Global Currency Reserve System. It’s a long read but absolutely recommended if you’re wondering why modern fiat currencies are so bad at holding value 💸💸

A smashing conversation between Demetri Kofinas and crypto villain (and possible JRR Tolkien character) Rohan Grey . The dude is a raging MMTer but sure has plenty of interesting takes and opinions about government, money and crypto. And don’t miss the second part!

_______________

See you next weekend for more insights.

Until then,

🦁